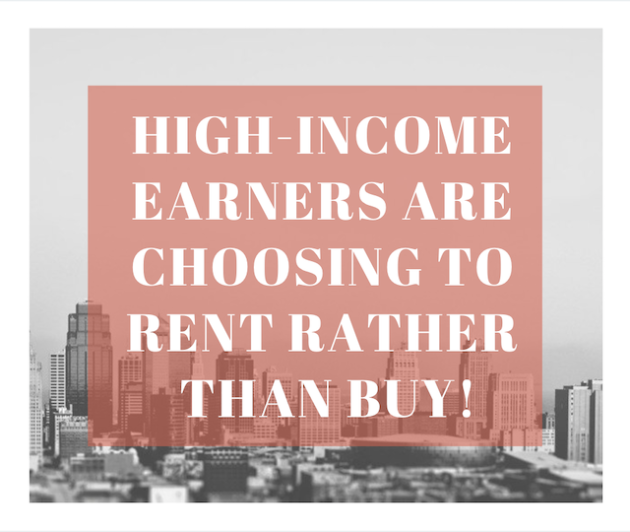

According to a recent article on CurbedLA, more than 450,000 high income earning (those making over $100,000 annually) individuals in Los Angeles are choosing to rent instead of buying as of 2017. A 30 percent jump when compared to 2008!

Part of the reason could be attributed to the decline of inventory for sale that would appeal to the financially stable young professional. Middle to high-income renters in Los Angeles no longer recognize buying as a feasible option. At The Rental Girl we often hear renters saying that they are priced out and will never be able buy in LA.

“Since 2008, “mortgage credit requirements have become more stringent, incomes have risen, but at a slower rate than home prices, and particularly for younger Americans, student-loan debt is making it difficult to save for a down payment,” writes Apartment List researcher Rob Warnock.

Stowing away funds for a down payment can be especially tricky in Los Angeles County, where the median home price was $581,500 in December. That means a traditional 20 percent down payment would be $116,300—a nearly impossible amount to set aside without a very hefty salary.”-CurbedLA

The Rental Girl has recently started selling apartments as Tenants-in-Common (TIC). At 10-20% less than comparable condos, TIC sales are a more affordable, and a excellent opportunity for renters to start building wealth through equity and homeownership. The TIC market is meeting a need of mid-to-high income earners who may otherwise feel priced out of Los Angeles.

Check out the full article for more details and the full article!